Foreclosure can feel overwhelming.

For many homeowners in North Carolina, it starts quietly:

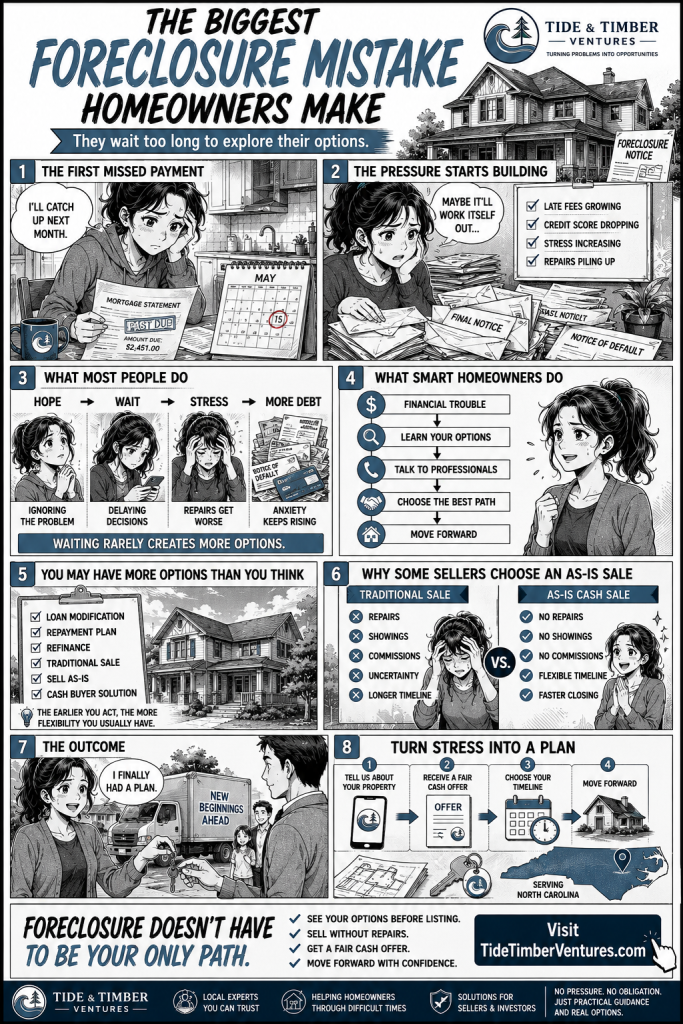

A missed payment.

A financial setback.

An unexpected life event.

Then the notices begin arriving, the pressure builds, and uncertainty takes over.

The good news is this:

You usually have more options than you think.

Understanding how foreclosure works in North Carolina can help you make informed decisions before the situation becomes more difficult or expensive.

Foreclosure is the legal process lenders use when a homeowner falls behind on mortgage payments.

If payments remain unpaid long enough, the lender may attempt to sell the property to recover the remaining loan balance.

In North Carolina, most foreclosures are handled through a non-judicial foreclosure process, which is generally faster than court-based foreclosure states.

That means timelines can move quickly once the lender begins formal action.

Most lenders begin contacting homeowners after the first missed payment.

At this stage:

Many homeowners try to catch up during this phase, but financial pressure often continues building.

If payments continue falling behind, the lender may issue a formal notice indicating the loan is in default.

This is a serious stage because legal foreclosure proceedings may begin shortly afterward.

At this point, homeowners often start exploring options like:

North Carolina commonly uses a power-of-sale foreclosure process.

A hearing may be scheduled before the clerk of court to determine whether the lender has the legal right to proceed.

If approved, the foreclosure sale can move forward relatively quickly.

The property may then be auctioned publicly.

If the home sells:

If nobody purchases the property, the lender may take ownership.

After foreclosure, homeowners may eventually be required to vacate the property.

The timeline varies depending on the situation, but this stage often creates additional emotional and financial stress.

Many homeowners wait too long because they hope the situation will improve on its own.

Common warning signs include:

The earlier you explore options, the more flexibility you usually have.

Every situation is different, but common solutions may include:

Some lenders may adjust loan terms to reduce payments.

A structured catch-up schedule may be available.

Possible in limited situations depending on equity and credit.

Works best for updated homes with enough equity and time.

Some homeowners prefer a faster, simpler solution to avoid foreclosure timelines entirely.

For sellers facing foreclosure pressure, traditional listings can sometimes create more delays.

Selling directly to a local cash buyer may help homeowners:

At Tide & Timber Ventures, we work with homeowners throughout the Carolinas who need straightforward solutions for difficult property situations.

We buy houses as-is and work on timelines that fit real-life situations whenever possible.

Transparency matters.

A direct cash sale may not be the best fit if:

Our focus is helping homeowners who value:

Here are several official and educational resources that may help:

Many foreclosure situations become harder simply because homeowners wait too long before exploring solutions.

Even if you’re unsure what direction to take, gathering information early can give you more control and more options.

If you’re dealing with foreclosure concerns in Charlotte or surrounding areas, you can learn more here:

No pressure. No obligation. Just practical guidance and real options for homeowners navigating difficult situations.

Mailing Address

1233 The Plaza 5545, Charlotte, NC, 28299